Are Tax Deductions for College Athletics Worth the Price?

Blog Post

Oct. 8, 2007

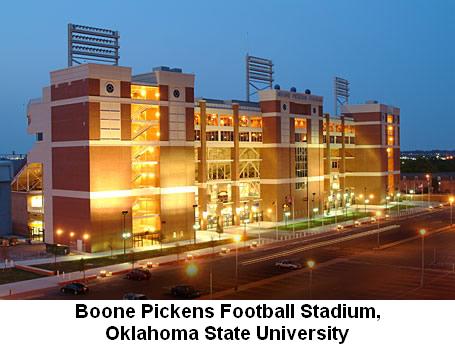

Last year, oil tycoon T. Boone Pickens broke the all-time record for gift-giving to a university athletics program when he donated $165 million to Oklahoma State University, his alma mater. Not only did OSU's sports program benefit, but Pickens himself received a large subsidy from the government because he was able to deduct that contribution from his income taxes.

Donations to college athletics programs are tax-exempt because government officials have long believed that college sports contribute to the educational purpose of higher education. When alumni give money to sports, the theory goes, they are contributing to students' educational experience beyond the classroom.

Donations to college athletics programs are tax-exempt because government officials have long believed that college sports contribute to the educational purpose of higher education. When alumni give money to sports, the theory goes, they are contributing to students' educational experience beyond the classroom.

But does the theory match reality? That's certainly a debatable point when you look at where Pickens' money is going. Much of his donation has been earmarked for facilities construction and improvement to the giant football stadium that already bears his name a new football turf, a spruced-up locker room, and most importantly a new brick exterior. His contribution will also pay for building a 100-acre athletic village to house Olympic-type sports facilities (displacing 1,300 local residents, according to the Wall Street Journal), plus a new equestrian center, a baseball stadium, and outdoor practice fields. Of course, OSU already has most of these things, but now it will have new shinier oneswhich, of course, the educational experience wouldn't be the same without!

The question of whether contributions to college athletic programs should be tax deductible is not just academic. According to the Chronicle of Higher Education, the largest athletics departments raised more than $1.2 billion from alumni in 2006-2007 for multimillion-dollar facilities and seven-figure coaches salaries. The enormous success in athletics fundraising efforts, however, may be coming at a cost. Alumni giving for academic programs at Division I-A schools has been stagnant in recent years. As a result, the Chronicle found that "contributions to sports programs are eating up an ever-larger share of donations to colleges," from 14 percent at these schools in 1998 to 26 percent in 2003.

This begs the question: is this $1.2 billion taxpayer-supported revenue stream furthering the educational, tax-exempt purpose of higher education? And if not, might contributions to academic programs increase if the tax deduction for athletics wasn't available?

College officials generally argue that increased spending on athletics, and in turn winning sports teams and increased school visibility, translate into satisfied alumni and more donations for the school overall. Unfortunately, this "happy alumni" hypothesis doesnt appear to hold true. Studies of alumni giving have found that winning sports teams dont have a significant effect on collegesand even in situations when donations do increase, they are typically athletic donations, not general academic donations.

There's also another type of tax-deductible athletics donation to consider: those that provide alumni with direct, personal benefits, such as skyboxes or courtside seats at sporting events. Most big-time sports schools require ticket holders to make a large athletics contribution in order to even get the right to purchase tickets. Donors are allowed to deduct 80 percent of that contribution (because somehow the IRS arbitrarily decided their personal benefit is worth 20 percent?). For example, the University of Texas sells private suites to its football games for $50,000 to $80,000. Somehow we dont think these donors are too concerned about the educational purpose of college athleticsor the fact that they get a tax deduction for it.

Can you imagine what even a small portion of the $50 million raised for athletics last year by the University of North Carolina at Chapel Hillthe most in the countrycould do for academics? In place of basketball coach Roy Williams $1.6 million salary, you could hire 12 full, tenured professors. You could build four new Institutes for Arts & Humanities with only half of UNCs annual athletics fund-raising total. [Disclosure: The author graduated from Duke University.]

To be fair, not all schools are spending their donations frivolously on extravagant facilities and preposterously high coaches salaries. Most Division I-A athletics programs operate at a deficit, and generally only the top-tier schools have millions of dollars to spend.

But theres definitely room to question whether taxpayers should be subsidizing Pickens pet athletic projects, or the tickets for luxury skyboxes at football stadiums. Last year, Congressspecifically Rep. Bill Thomas (R-CA) and the House Committee on Ways and Meansstarted to investigate the tax-exempt status of NCAA sports. Thomas sent a harshly worded letter to the NCAA requesting information, and was planning a hearing, which never transpired.

However interest may be growing again in Congress. After seeing the Chronicle article about athletics donations crowding out academic donations, Sen. Charles Grassley (R-Iowa) said in a written statement: "When I hear stories about top donors to college athletic programs getting a free seat on the team plane, I wonder what the public gets out of that. We need to make sure that taxpayer subsidies for college athletic-program donations benefit the public at large."

Grassley hit the heart of this issue: What is the public getting out of subsidizing athletics donations? We will return to this question, and others surrounding the NCAAs tax-exempt status, in the future.