CBO Issues Fresh Evidence That Student Loan Defaults Cost Taxpayers

Blog Post

July 30, 2012

Ed Money Watch has run a number of posts over the past two years debunking the myth that the federal government profits when borrowers default on their student loans (see here and here). This well-worn myth holds that the penalties, fees, and interest the government charges defaulters, coupled with its extraordinary collection powers (tax refund offset, wage garnishment, etc.) means the government stands to collect more on a student loan when a borrower defaults than if he had paid it off in full and on time. This simply isn’t true – and new evidence that it is not was just released.

Back in February, the U.S. Department of Education buried a table in hundreds of pages of budget documents illustrating that after netting out what the government spends to collect on a defaulted student loan, and adjusting for the risk-free time-value off money, the government ultimately collects 80 cents on the dollar on a loan that defaults. Now comes more evidence from the Congressional Budget Office that defaults are costly for taxpayers.

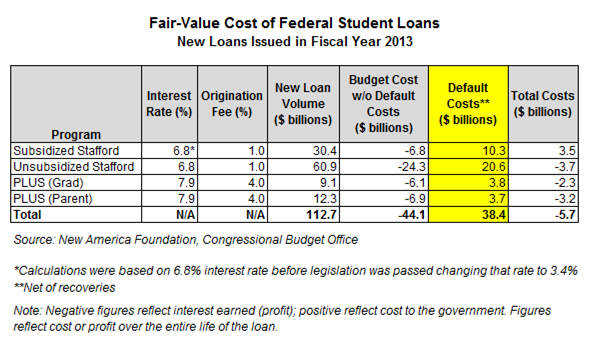

In a recent paper, “Fair Value Estimates of the Cost of Federal Credit Programs in 2013,” the CBO published a spreadsheet detailing the component parts of its cost estimates for federal student loans issued for the upcoming school year. Among those pieces is the effect that defaults on newly-issued student loans have on the cost of the program.

If the myth of the profitable student loan default were true, the CBO spreadsheet would show that defaults reduce the estimated cost of newly-issued loans. But estimates show just the opposite: Losses from defaults are the costliest part of the federal student loan program.

The table above uses information from the CBO loan costs spreadsheet to show the total losses from defaults that the agency estimates the government will incur on loans issued during fiscal year 2013 (October 1, 2012 to September 30, 2013). The costs are “net of recoveries,” or the amount of a loan that the agency estimates the government will not be able to recover from borrowers who default, and they reflect a risk-adjusted time value of money. (In CBO’s words, it is “the subsidy component due to default losses [which] represents the present value of defaults net of recoveries.”)

The highlighted column in the table shows the cost of defaults. For Unsubsidized Stafford loans, the most widely-available federal student loan, defaults are expected to cost taxpayers $20.6 billion over the life of the loans. Subsidized Stafford loan defaults will cost $10.3 billion, and even PLUS loans made to graduate students (theoretically the lowest-risk borrowers) are expected to impose $3.8 billion in default losses on taxpayers. In total, using fair-value estimates, CBO expects that of the $112.7 billion in newly-issued student loans the government will make this coming year, just over $38.4 billion will be lost to defaults even after the government collects whatever it can on the defaulted loan.

Be aware that the $38.4 billion is not the total cost of the loans – it is only the gross cost of defaults, net of collections. The last column in the table shows the total cost of the loan program, which combines losses from defaults with interest payments from all student loans. For all loans except Subsidized Stafford loans, the default losses are more than offset by the interest that borrowers will pay on their loans.

In short, the latest figures from the Congressional Budget Office show that student loan defaults are not a money-maker for the government. In fact, if no borrower ever defaulted or if the government successfully collected every unpaid dollar in a default immediately and at no cost, the federal student loan program’s costs would go down by $38.4 billion.