Did Congress Cut Interest Rates on the Wrong Student Loans?

Blog Post

June 28, 2012

Congress and the president are about to get an earful from angry college students and parents. Lawmakers just cut the interest rate on the wrong type of federal student loans. At least, that’s one take on a new Congressional Budget Office (CBO) report.

The CBO announced yesterday that most federal student loans made this coming school year will charge interest rates high enough to earn the government a profit. The only exception: Subsidized Stafford loans for undergraduates. Those loans still provide enough benefits to borrowers to show a cost to the government – and that was before Congress and the president agreed to cut the interest rate on those loans to 3.4 percent for another year.

Yes, the federal student loan program has always appeared profitable, but those profits were the result of an accounting bias written into federal law. The profits were, in other words, fictitious. The CBO endorsed that view earlier this year, and says that the federal law that forces it to exclude costs for all of the risks inherent in government loan programs thereby understates costs. To compensate for that bias, the CBO prefers fair-value estimates, which include a cost for all risks. Until now, those estimates have shown that the federal student loan program charges interest rates low enough to impose costs on taxpayers. In 2010, the last time it calculated such figures, the agency showed that the average direct loan cost $12 for every $100 lent. In other words, the loans provided subsidies to borrowers.

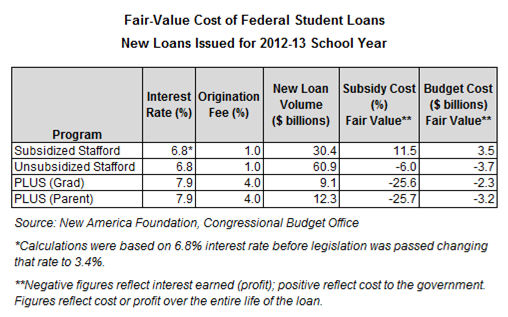

According to CBO’s new estimate, that won’t be the case for the vast majority of federal student loans issued this coming school year. New fair-value estimates show that three types of federal student loans (Unsubsidized Stafford, Parent PLUS, and Grad PLUS) are expected to earn a profit for the government. Subsidized Stafford loans, however, would still provide a subsidy to borrowers (and impose a cost on taxpayers) due to their interest-free benefit and default rate in excess of 20 percent. That subsidy will be even larger than the CBO estimates show now that the 3.4 percent interest rate is extended.

While it should be uncommon for government loan programs to show profits using fair-value estimates, it’s not difficult to see why this year’s loans do. As many know, interest rates on all types of loans in the market have fallen to record lows. In mid-2011 and early 2012 long-term rates moved sharply lower, and the high-risk premiums lenders charged during the recession are mostly gone. Yet Congress has kept the fixed interest rates on newly-issued student loans at the rates lawmakers chose back in 2001. So a Parent PLUS loan issued today still charges a fixed rate of 7.9 percent (with a 4.0 percent origination fee) and an Unsubsidized Stafford loan still charges 6.8 percent (with a 1.0 percent origination fee) even in today’s low rate environment. (Congress’s and the president’s decision to eliminate graduate students from the Subsidized Stafford loan program also contributes to the program’s swing to profitability this year).

The table below shows the profit that the government will make on each type of loan issued this coming school year. The figures reflect the profit (or loss in the case of Subsidized Stafford loans) earned over the entire repayment period of the loan.

We should also point out that the CBO has a few caveats to its new numbers, excerpted below:

In principle, programs with a large negative fair-value subsidy [profit for the government] should be rare, because a negative fair-value subsidy should represent a profitable opportunity for a private financial institution to provide credit on the same or better terms. However, a negative fair-value subsidy could arise, for instance, if there are barriers to entry—such as the need for private lenders to incur large fixed costs to enter a particular credit market—and if the profit opportunity is expected to be shortlived.

In other words, the government could earn a profit on loan programs and still provide the best deal around. Even so, the latest CBO numbers offer a compelling case for Congress to cut the interest rate on the three types of federal student loans expected to earn a profit – Unsubsidized Stafford, Parent PLUS, and Grad PLUS loans. Ironically, lawmakers are about to pass a bill that cuts the interest rate on none of those loans.

We at Ed Money Watch have proposed a simple and fair way to cut rates on all loans issued this coming year at no cost to taxpayers over the long term. If Congress sets a fixed interest rate on all newly-issued loans each year based on the interest rate on 10-year Treasury notes, plus 3.0 percentage points, rates would be set low enough to eliminate any profits for the government. And borrowers this coming school year would get loans at fixed rates of about 4.75 percent, based on Treasury rates last month.

Senators Coburn (R-OK) and Burr (R-NC) offered this plan in the Senate. Their fellow lawmakers and the president took a pass. Think about that. As the president and student aid advocates celebrate the 3.4 percent interest rate extension for some students, the government is set to earn a few billion dollars in profits off all other students and parents.